Brendan Burgess

Founder

- Messages

- 55,505

The fee to switch in contract takes the good out of it at the minute

What is the balance on your mortgage?

What fee are they quoting?

Which lender?

The fee to switch in contract takes the good out of it at the minute

Just to note that Euribor is set by the EMMI (European Money Markets Institute) and not the ECB but I guess it's strongly influenced by ECB rates.The tracker margin of 0.9% means that the rate will be set by the ECB for the full term of the mortgage and not by the banks' whim and caprice.

www.emmi-benchmarks.eu

www.emmi-benchmarks.eu

When fixed rate is over people should be shopping around - as I am doing now.

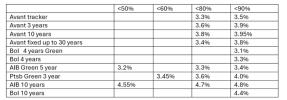

I think a fixed-rate of 3.4% for the lifetime of the mortgage, plus 1% cash back, is a better deal than the flex mortgage offering.

I wonder does Avant allow borrowers to split their mortgages between the different offerings?

I think a fixed-rate of 3.4% for the lifetime of the mortgage