Brendan Burgess

Founder

- Messages

- 55,242

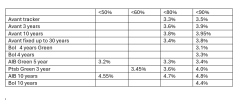

Avant launched a tracker in March which they call their "Flex Mortgage". Not sure why they don't call it a tracker.

It tracks the 1 year Euribor rate - which is very similar to the ECB rate which tracked by other mortgages.

The margin is fixed for the life of the mortgage - 0.9% for LTV <80% and 1.1% for LTV >80%

It has the huge advantage of a variable rate mortgage in that you can pay lump sums off it or clear it in full at any time, without penalty.

It has the huge advantage of a tracker in that the margin is fixed for the life of the loan. The bank can't set the rate at its own discretion. This is a particular problem in Ireland where banks have exploited people's reluctance or inability to move by having very high variable rates.

It tracks the 1 year Euribor rate - which is very similar to the ECB rate which tracked by other mortgages.

The margin is fixed for the life of the mortgage - 0.9% for LTV <80% and 1.1% for LTV >80%

It has the huge advantage of a variable rate mortgage in that you can pay lump sums off it or clear it in full at any time, without penalty.

It has the huge advantage of a tracker in that the margin is fixed for the life of the loan. The bank can't set the rate at its own discretion. This is a particular problem in Ireland where banks have exploited people's reluctance or inability to move by having very high variable rates.