Dan_The_Man

Registered User

- Messages

- 58

Any considerations with this one?

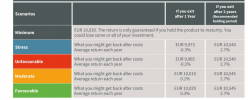

Term: 2 years

Capital Protection: 100%

Capital Protection Goldman Sachs Group Inc

Provider: (Moody’s: A2/S&P: BBB+/Fitch: A)

Fixed Return: 2.7% paid out at the end of each year regardless

to investment performance

Underlying Index: EuroStoxx 50 Index (SX5E Index)

Potential Return Additional return of 0.05% if EuroStoxx 50 Index is

at Maturity: at or above its initial level

Summary Risk

Indicator: 2

Minimum Return: 5.4%

Maximum Return: 5.45%

Minimum Amount: €100,000

Closing Date: 30 August 2023 (or earlier if fully subscribed)

Liquidity: Daily, via stock market listing

Taxation: Income Tax for Personal Investors

Availability: Personal: Conexim and Omnium Investment

Platforms

Pension: Self Administered and Self Directed

Insured Plans

Term: 2 years

Capital Protection: 100%

Capital Protection Goldman Sachs Group Inc

Provider: (Moody’s: A2/S&P: BBB+/Fitch: A)

Fixed Return: 2.7% paid out at the end of each year regardless

to investment performance

Underlying Index: EuroStoxx 50 Index (SX5E Index)

Potential Return Additional return of 0.05% if EuroStoxx 50 Index is

at Maturity: at or above its initial level

Summary Risk

Indicator: 2

Minimum Return: 5.4%

Maximum Return: 5.45%

Minimum Amount: €100,000

Closing Date: 30 August 2023 (or earlier if fully subscribed)

Liquidity: Daily, via stock market listing

Taxation: Income Tax for Personal Investors

Availability: Personal: Conexim and Omnium Investment

Platforms

Pension: Self Administered and Self Directed

Insured Plans