You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Key Post Ulster Bank mortgage customers should fix for as long as possible before ptsb buys the mortgage and bumps up the rate

- Thread starter SPC100

- Start date

Brendan Burgess

Founder

- Messages

- 52,099

maybe the advice should be dumbed down for most people

Hi SPC

You are probably right, but I hate doing that.

But here is my dumbed down version

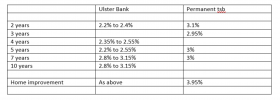

1) If can switch to another lender you should do so and not be taken over by permanent tsb by default, as you will be going from the cheapest lender to the dearest lender.

Full details here:

Key Post - Should an existing Ulster Bank customer do anything before their mortgage is sold to permanent tsb?

Ulster Bank is nearly the cheapest lender at the moment while permanent tsb is the most expensive. Anyone who moves to Ulster Bank who is not on a tracker will find themselves paying a lot more when they move to permanent tsb. If you have a cheap tracker with Ulster Bank, you don't need to do...

www.askaboutmoney.com

2) If you can't or won't switch because

- you are in arrears or have a bad credit record

- you are planning to trade up in the short to medium term

- you have only a few years left on your mortgage

- your mortgage balance is low

- you can't be bothered

Permanent tsb will be forced to respect the fixed rate.

Last edited:

Brendan Burgess

Founder

- Messages

- 52,099

Hi SPC

Just revisiting the thread on what Ulster Bank customers should do and I was thinking, this is a bit complex, when I came across your post - thus proving your point.

I have edited the second post accordingly.

Brendan

Just revisiting the thread on what Ulster Bank customers should do and I was thinking, this is a bit complex, when I came across your post - thus proving your point.

I have edited the second post accordingly.

Brendan

Last edited:

Brendan Burgess

Founder

- Messages

- 52,099

Brendan Burgess

Founder

- Messages

- 52,099

All customers can break out of an existing fixed rate at any time.

However, you may have to pay an early repayment fee.

It is very unlikely that Ulster Bank will waive this fee.

Brendan

However, you may have to pay an early repayment fee.

It is very unlikely that Ulster Bank will waive this fee.

Brendan

ethicaback

Registered User

- Messages

- 5

Hi Folks,

I just got this link from the Ulster bank app.

ulsterbank.ie/help-and-support/important-customer-notice.html

Something that was a bit concerning was this question and answer:

While we can reassure you that the 10% overpayment feature remains available and unchanged, we are unable to confirm until final arrangements are made with the new provider of your loan, whether this feature will continue unchanged when your mortgage is transferred. If you wish to make an overpayment, please log on to Manage My Mortgage

----

I just fixes for 4 years planning to use the 10% overpayment to reduce the mortgage when I can. I would be really disappointed if I remained locked into the 4 year term without the 10% overpayment option if PTSB said they would not honour it. Could it be grounds to break out of the fixed term without penalty?

I just got this link from the Ulster bank app.

ulsterbank.ie/help-and-support/important-customer-notice.html

Something that was a bit concerning was this question and answer:

---

Will I be able to avail of the 10% overpayment feature on my fixed rate when my mortgage is transferred to a new providerWhile we can reassure you that the 10% overpayment feature remains available and unchanged, we are unable to confirm until final arrangements are made with the new provider of your loan, whether this feature will continue unchanged when your mortgage is transferred. If you wish to make an overpayment, please log on to Manage My Mortgage

----

I just fixes for 4 years planning to use the 10% overpayment to reduce the mortgage when I can. I would be really disappointed if I remained locked into the 4 year term without the 10% overpayment option if PTSB said they would not honour it. Could it be grounds to break out of the fixed term without penalty?

It's been a number of years since i last looked at my Ulster Bank contract so I'm open to corrections but I feel the 10% overpayment wasnt explicit in it.

Even if it were you'd have to check that there wasn't a subsequent clause in the mortgage contract stating that they can remove the option in the event that they sell the loan.

I imagine given the wording on the website it's the banks view that there is a sufficiently grey area that we end up waiting another decade to find out who's interpretation is correct.

While I appreciate not everyone is in a position to switch, the fact that other lenders offer the same 10% annual overpayment option and do so with lower rates means people should consider switching.

The only people who shouldn't bother are those with sufficiently low balances where the cost of switching would out way the benefits of lower rates.

Even if it were you'd have to check that there wasn't a subsequent clause in the mortgage contract stating that they can remove the option in the event that they sell the loan.

I imagine given the wording on the website it's the banks view that there is a sufficiently grey area that we end up waiting another decade to find out who's interpretation is correct.

While I appreciate not everyone is in a position to switch, the fact that other lenders offer the same 10% annual overpayment option and do so with lower rates means people should consider switching.

The only people who shouldn't bother are those with sufficiently low balances where the cost of switching would out way the benefits of lower rates.

Last edited:

That's the key question - is the ability to overpay on a fixed rate mortgage, without penalty, specified in the Ulster Bank loan agreement?

- if it is, its contractual and the party taking on the loans will have to honour it

-if its not expressly stated, then forget it.

- if it is, its contractual and the party taking on the loans will have to honour it

-if its not expressly stated, then forget it.

That is a very good point. I've gone through my documentation and while the 10% overpayment ability is mentioned in the welcome letter, it says nothing about it being penalty free, just that it is possible. So far I'm not found any other reference to it in any of the other documents.

Brendan Burgess

Founder

- Messages

- 52,099

That's the key question - is the ability to overpay on a fixed rate mortgage, without penalty, specified in the Ulster Bank loan agreement?

- if it is, its contractual and the party taking on the loans will have to honour it

-if its not expressly stated, then forget it.

I am not convinced of this.

For example, most of the customers who got tracker redress would have got nothing if they relied on their contract. The Central Bank required them to look at all the marketing material as well.

Likewise, the Ombudsman would look very dimly on Ulster Bank if they advertised 10% overpayments without penalty but the contract said something else.

ptsb would be very stupid to charge an early break fee on Ulster Bank customers who overpay 10%. And I would be fairly sure that the Ombudsman would uphold a complaint on the issue.

@ethicaback Don't worry about it for now. Do carefully keep any correspondence or marketing material you have which shows that you chose Ulster Bank because of this. Even keep a copy of that website FAQ. Just in case ptsb do something stupid.

Brendan

ethicaback

Registered User

- Messages

- 5

Thanks for the advice folks.

For anyone else in the same situation I used the following search terms to find public pages on google where UB state the 10% overpayment feature. It could be useful to save the pages as PDF as Brendan mentioned:

For anyone else in the same situation I used the following search terms to find public pages on google where UB state the 10% overpayment feature. It could be useful to save the pages as PDF as Brendan mentioned:

Code:

overpayment 10% site:ulsterbank.ie

overpayment 10% ulsterbank filetype:pdfBrendan Burgess

Founder

- Messages

- 52,099

have a fixed rate expiring in September 2022, (it should expire in may 2022 but that's another story), does anyone know at what rate PTSB will get these mortgages, will I have the opportunity in about 12 months time to re fix with UB or will my mortgage be with PTSB in 1 year?, anyone any thoughts on how long this process will take?

Given that they've only recently managed to sign a memorandum of understanding, so have yet to finalise a commercial agreement, and then they need to obtain regulatory approval - and then, assuming approval, they need to physically migrate the loans over to PTSB, I think you'll still be an Ulster Bank customer in a year's time tbh (perhaps not much longer than a year's time though).

That's just my personal opinion though, there are no guarantees")

That's just my personal opinion though, there are no guarantees

boilerstove

New Member

- Messages

- 4

While I appreciate not everyone is in a position to switch, the fact that other lenders offer the same 10% annual overpayment option and do so with lower rates means people should consider switching.

The only people who shouldn't bother are those with sufficiently low balances where the cost of switching would out way the benefits of lower rates.

UB allows you to overpay by 10% of the total owed per month.

So if I have a mortgage of 200k, I could in theory make an overpayment of 20k in the first year.

Most other 10% Overpayments are on the month owed, so if my monthly mortgage was 1000e, I can only overpay by 100e.

Open to correction here though because the UB 10% overpayment is what's keeping me there...

Per year.UB allows you to overpay by 10% of the total owed per month.

No. That's Bank of Ireland only.Most other 10% Overpayments

Anyone else that allows overpayment, wurhout calculating a break fee, is based on balance.

boilerstove

New Member

- Messages

- 4

Correct on the per year RedOnion.

Really? Good to know, so no reason really to stay with UB then?

Really? Good to know, so no reason really to stay with UB then?