Brendan Burgess

Founder

- Messages

- 55,351

Update ; Sept 2024. I am updating this based on S Class's work and my own experience.

I will try to do an Idiot's Step by Step Guide on how to reclaim the tax.

When you get a dividend from a German company through your Irish stockbroker, you should get a dividend certificate as follows:

The German tax of 26.375% is based on 2023 dividends. I think this rate has been different in the past.

On your tax return, you declare a gross income of €100 and pay Income Tax, USC and PRSI on that as normal, but you claim credits as follows:

On your Irish Tax Return

You can reclaim some more from the German Revenue

I don’t know where the figure of 26.375% came from – it’s an Income Tax and a Solidarity Tax.

I don’t think you get the full 11.375% back. They don’t give you the Solidarity Tax.

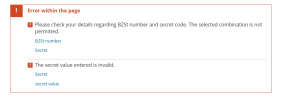

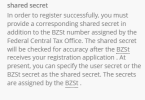

To claim the German tax - Work in Progress

See below for links and detailed instructions.

You must claim it by the end of the fourth calendar year following that in which the dividends and/or interest have been received.

So for Dividends received in 2020, the claim must be submitted by the end of 2024.

I will try to do an Idiot's Step by Step Guide on how to reclaim the tax.

When you get a dividend from a German company through your Irish stockbroker, you should get a dividend certificate as follows:

The German tax of 26.375% is based on 2023 dividends. I think this rate has been different in the past.

On your tax return, you declare a gross income of €100 and pay Income Tax, USC and PRSI on that as normal, but you claim credits as follows:

On your Irish Tax Return

- You get the encashment tax of €17.375 back in full

- You can claim 15% or €15 as a credit

You can reclaim some more from the German Revenue

I don’t know where the figure of 26.375% came from – it’s an Income Tax and a Solidarity Tax.

I don’t think you get the full 11.375% back. They don’t give you the Solidarity Tax.

To claim the German tax - Work in Progress

See below for links and detailed instructions.

You must claim it by the end of the fourth calendar year following that in which the dividends and/or interest have been received.

So for Dividends received in 2020, the claim must be submitted by the end of 2024.

Last edited: