Diane mc Manamo

Registered User

- Messages

- 12

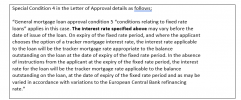

Hi there im very new to this but im looking for advise. I took out a mortgage in 2007 on my own and signed for a tracker mortgage. I was only 23 so i had the option to fixed it for 5 yrs which i did in 2012 i received a letter saying my 5 yr fixed is due to end and i can fix again or go onto a variable rate. I contacted the bank and was told tracker was now no an option as they were withdrawn. My loan offer states i signed for tracker

Kind regards Diane

Kind regards Diane

Last edited by a moderator: