The Evolution of Irish Household Wealth | Central Bank of Ireland

This behind the data publication focuses on the evolution of Irish household wealth inequality since 2013

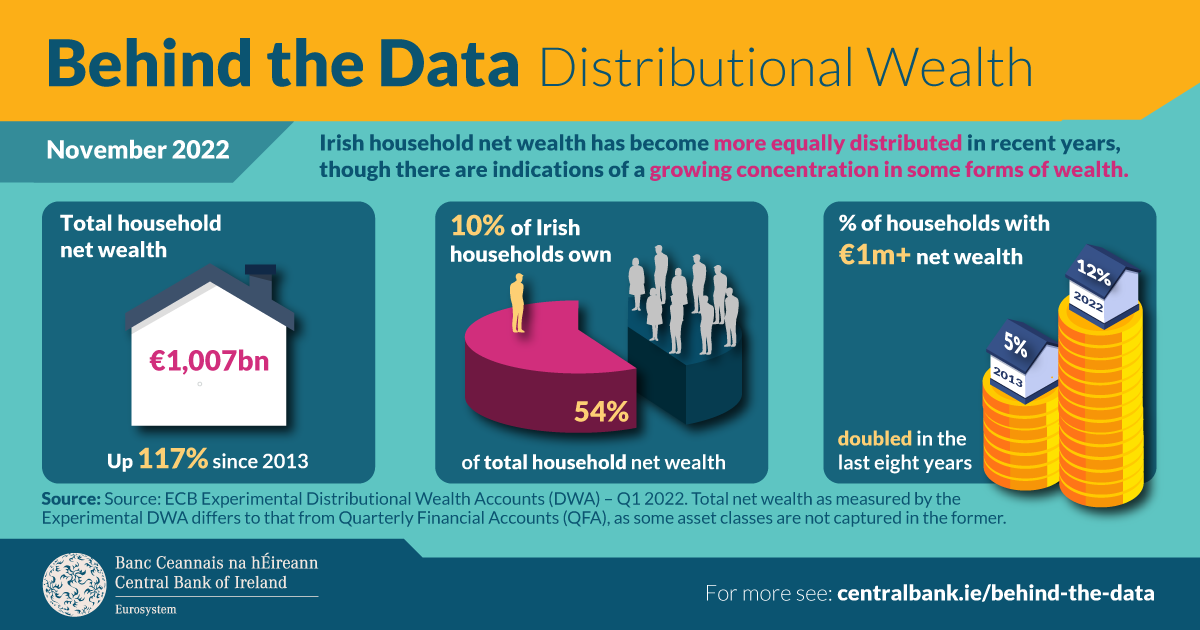

Another interesting nugget from the analysis is that the % of total household net wealth owned by the top 10% of Irish households has actually fallen from 60% in 2013 to 54% in 2022.

It's a pity, IMO, that the data isn't broken down into age cohorts. I suspect the proportion of households headed by somebody in their 60s with net wealth of €1m+ is actually quite significant, whereas I suspect very few households headed by somebody in their 30s have net wealth of €1m+.

Another weakness of the data, IMO, is that it excludes claims on the State in calculating net wealth. For example, the average Garda would have accrued pension entitlements with an actuarial value well north of €1m by 55 but that doesn't show up in data.