Brendan Burgess

Founder

- Messages

- 55,428

this needs to be updated. AIB is now charging exorbitant rates for customers who don't have green mortgages, so they are no longer a recommended lender. Brendan 28th March 2025

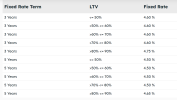

When choosing a lender, it's important not to just pick the one with the lowest rate today.

I would recommend AIB or Avant as the lenders most likely to be the best value over the full term of your mortgage.

AIB has a long history of treating customers fairly when it comes to mortgage rates

I would avoid Bank of Ireland and ptsb as they attract new customers with tricks but are likely to be poor value over the full term of your mortgage.

When choosing a lender, it's important not to just pick the one with the lowest rate today.

I would recommend AIB or Avant as the lenders most likely to be the best value over the full term of your mortgage.

AIB has a long history of treating customers fairly when it comes to mortgage rates

- They allow existing customers to avail of the best rates offered to existing customers

- They have a comparatively low variable rate

- They do not engage in gimmicks to trick customers.

- I would expect their rates to be competitive over the longer term

- They cap the early repayment fee at 2%

- They allow 10% overpayment of a fixed rate each year without penalty.

I would avoid Bank of Ireland and ptsb as they attract new customers with tricks but are likely to be poor value over the full term of your mortgage.

- They attract new customers with lower rates which they do not allow existing customers to avail of

- They keep their variable rates artificially high

- Many customers default to variable rates when their fixed rates end and don't do anything about it

- High variable rates mean you are forced to fix which means you are , in effect, forced to stay with them for another few years and stuck on a higher rate than new customers

- They engage in all sorts of gimmicks to trick customers

- For example, Bank of Ireland offers a green discount to new customers. But when the fixed rate period is up, you are an existing customer and no longer qualify for the green discount.

- Some of their rates for large mortgage apply to new mortgages only, so you get that rate only for the firs period of fixing.

- ptsb, in particular, has a long history of exploiting vulnerable customers and although you are in a good position now, you could be vulnerable at some stage over the next 20 years.

- They offered attractive looking "discounted trackers" to customers at a rate of 0.8% above the ECB rate for the first year. When the first year was up, they were put on ECB +3.25%.

- Customers who were entitled to trackers when fixed rates ended, were offered variable rates pitched just below the tracker rate. Most customers opted for these, little knowing that once they were off their trackers, ptsb hiked the variable rate.

- During the financial crisis, when AIB and BoI had a standard variable rate of 3% and 3.5% , ptsb were charging over 6% and most customers could not switch as the market had frozen.

- For a long time, ptsb did not even allow existing customers to fix at any rate, forcing them to pay high variable rates. And when they did introduced fixed rates for existing customers, they were substantially higher than the rates on offer to new customers.

Last edited: