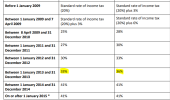

As the rate increased they kept the same +3% until they both were raised to 41%, so the equivalent now would be 36%.There used be 20% CGT tax and 23% tax on funds to account for rolled up dividends.

If we assume they didn't pull the 23% figure out of the air, then a proportional figure based on 33% CGT would be, if I've calculated correctly, 38%.

But that's irrelevant - the report already recommends 33%, why propose a higher rate?