You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

How much 'should' you have in a pension at age 50?

- Thread starter spicyone

- Start date

I don't think there is a universally "right" answer to this question but I have seen it recommended, as a guide, that you "should" have six times your salary saved by age 50 and ten times your salary saved by 65.

But I would take those recommendations with a big pinch of salt.

But I would take those recommendations with a big pinch of salt.

It also depends on when you want to drawdown, what the market returns will be like between now and then, how much you're contributing on an on-going basis etc.

To least to give you one answer

Let's assume, 65 drawdown, target pot of 2m, you're contributing 1k a month & you get a return of 5.5% over those 15 years. The answer would be approx 750k at 50.

To least to give you one answer

Let's assume, 65 drawdown, target pot of 2m, you're contributing 1k a month & you get a return of 5.5% over those 15 years. The answer would be approx 750k at 50.

Dr Strangelove

Registered User

- Messages

- 2,286

That’s far in excess of the lifestyle needs of a typical person, particularly if you have a contributory pension and a house without a mortgage.target pot of 2m,

Gordon Gekko

Registered User

- Messages

- 7,936

It is ‘only’ €60,000 a year, in a world where inflation is back on the agenda. Not to be sniffed at, and probably €73,000 in total, but not huge either, particularly if it’s to cover a couple.That’s far in excess of the lifestyle needs of a typical person, particularly if you have a contributory pension and a house without a mortgage.

It should never be to cover a coupleIt is ‘only’ €60,000 a year, in a world where inflation is back on the agenda. Not to be sniffed at, and probably €73,000 in total, but not huge either, particularly if it’s to cover a couple.

Dr Strangelove

Registered User

- Messages

- 2,286

Well two people do cost more than one…..Not to be sniffed at, and probably €73,000 in total, but not huge either, particularly if it’s to cover a couple.

Average full-time earnings of workers are around €50k so retirement income of €73k is a multiple of a typical retiree’s income.

Gordon Gekko

Registered User

- Messages

- 7,936

Perhaps. But I suspect that the average earnings of someone seeking advice and/or an Askaboutmoney member are higher.Well two people do cost more than one…..

Average full-time earnings of workers are around €50k so retirement income of €73k is a multiple of a typical retiree’s income.

The key point is that €60,000 a year won’t be worth anywhere near as much by the time the person planning today gets to drawdown their pension fund in the future.

Dr Strangelove

Registered User

- Messages

- 2,286

I agree. But inflation helps with accumulation as well as meaning more of a drawdown.The key point is that €60,000 a year won’t be worth anywhere near as much by the time the person planning today gets to drawdown their pension fund in the future.

Gordon Gekko

Registered User

- Messages

- 7,936

Except there’s a cap of €2m which is designed to cap the pension at €60k. The €2m should be index linked as was the case in the past.I agree. But inflation helps with accumulation as well as meaning more of a drawdown.

Steven Barrett

Registered User

- Messages

- 5,461

I think limiting yourself to just looking at your pension value is incorrect (and that's coming from a pension advisor!), you should look at your overall wealth and pensions is just a strand of that. If you have a small pension but a load of debt free investment properties, you will also be in a good position to fund your retirement.

a method of assessing your wealth is age x income / 10. If it's a couple, do the calculation for both and add together. deduct any inheritance from the calculation.

Steven

http://www.bluewaterfp.ie (www.bluewaterfp.ie)

a method of assessing your wealth is age x income / 10. If it's a couple, do the calculation for both and add together. deduct any inheritance from the calculation.

Steven

http://www.bluewaterfp.ie (www.bluewaterfp.ie)

Gordon Gekko

Registered User

- Messages

- 7,936

For what it’s worth, I find it more helpful to work out my requirements excluding debt and retirement provision in today’s terms and then applying an inflation rate to that to work out what I think I’ll need. Then build in some fat, then work out what’s needed to deliver that.

coolaboola12

Registered User

- Messages

- 323

most of these calculators talk about having a pension pot so large that you can have a safe withdrawl rate and the fund itself will last forever. I dont see the point of this, no one will live forever and you would end up leaving a massive amount of money after you

time to plan

Registered User

- Messages

- 910

As always you have to look at the big picture of your total pension entitlements. As an example, in my case, I only started paying into a pension at 50, but am piling cash in at 42k per year as a proprietary director. I won't be fussed about a safe withdrawal rate as the big picture is that my wife amd I both have UK and Irish state pensions, I have a small but not trivial NHS pension and my wife has a similar UK University scheme pension and is now building up an Irish public sector pension.most of these calculators talk about having a pension pot so large that you can have a safe withdrawl rate and the fund itself will last forever. I dont see the point of this, no one will live forever and you would end up leaving a massive amount of money after you

So if I end up over-withdrawing on my pension fund, the impact of it is not catastrophic as it could be on an individual or couple entirely reliant on it and an Irish state pension.

Blackrock1

Registered User

- Messages

- 1,778

what do you mean Steven? are you saying if you are 40 and earn 200k you should have 800k in assets or am i misunderstanding?I think limiting yourself to just looking at your pension value is incorrect (and that's coming from a pension advisor!), you should look at your overall wealth and pensions is just a strand of that. If you have a small pension but a load of debt free investment properties, you will also be in a good position to fund your retirement.

a method of assessing your wealth is age x income / 10. If it's a couple, do the calculation for both and add together. deduct any inheritance from the calculation.

Steven

http://www.bluewaterfp.ie (www.bluewaterfp.ie)

Would you include equity in your home as wealth? Or just pension and any investments?I think limiting yourself to just looking at your pension value is incorrect (and that's coming from a pension advisor!), you should look at your overall wealth and pensions is just a strand of that. If you have a small pension but a load of debt free investment properties, you will also be in a good position to fund your retirement.

a method of assessing your wealth is age x income / 10. If it's a couple, do the calculation for both and add together. deduct any inheritance from the calculation.

Steven

http://www.bluewaterfp.ie (www.bluewaterfp.ie)

Steven Barrett

Registered User

- Messages

- 5,461

That's correct. It is a rule of thumb from The Millionaire Next Door.what do you mean Steven? are you saying if you are 40 and earn 200k you should have 800k in assets or am i misunderstanding?

Age x realised pretax annual household income from all sources except inheritances. Divide by 10. This, less any inherited wealth is what your net worth should be.

To be well positioned PAW (prodigious accumulator of wealth), you should be two times the expected level of wealth.

The book doesn't say specifically but I include the net value of your home. I know some people exclude the value of the home when assessing net worth as you need somewhere to live.Would you include equity in your home as wealth? Or just pension and any investments?

At the end of the day, it's a largely meaningless exercise when viewed in isolation. Your spending habits and what you want to do in life also has to be taken into account. You have 4-5 kids that will leave home for 3rd level and you want to help them get them on the property ladder as well as you wanting to retire early, buy a holiday home etc. That's going to cost you a lot of money and the big pot you have may not last as long as you think it will.

I find if people have good saving habits throughout their life, they do alright. Make pension and savings automatic and don't get into too much debt.

Steven

http://www.bluewaterfp.ie (www.bluewaterfp.ie)

Steven

http://www.bluewaterfp.ie (www.bluewaterfp.ie)

Steven Barrett

Registered User

- Messages

- 5,461

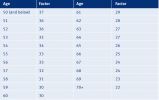

It used to be multiply it by 20. It's changed now and you multiply it by a factor depending on what age you retire. Doesn't really reflect the true value of a DB pension but then, you can only know the true value of it based on the annuity rates in the market at the time of retirement.is it possible to calculate a defined benefit pension worth? i have no idea what it will be worth or what it is worth now!