Brendan Burgess

Founder

- Messages

- 55,609

Update: I have changed my mind on this in the light of the comments by Red Onion and Sarenco on break fees. People should fix now. Brendan 18th December 2017

I don't think it's a good idea for anyone to fix at present. While ECB rates will rise at some stage, Irish mortgage rates are too high, and should fall before the ECB rates rise.

Having said that,

It may be much cheaper than you think to break out of a fixed rate early...

After Irish rates have fallen, fixing might well be worth considering.

So it seems to me that the best options at present are either an EBS variable rate with 2% cash back or the KBC mortgage with €3,000 cash back.

Then switch to another lender after a few months and get more cash back.

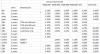

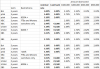

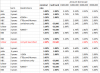

But as a lot of customers want to fix, here is a schedule of the Best Buys, after incorporating the cash backs.

I don't think it's a good idea for anyone to fix at present. While ECB rates will rise at some stage, Irish mortgage rates are too high, and should fall before the ECB rates rise.

Having said that,

It may be much cheaper than you think to break out of a fixed rate early...

After Irish rates have fallen, fixing might well be worth considering.

So it seems to me that the best options at present are either an EBS variable rate with 2% cash back or the KBC mortgage with €3,000 cash back.

Then switch to another lender after a few months and get more cash back.

But as a lot of customers want to fix, here is a schedule of the Best Buys, after incorporating the cash backs.

Last edited: