9thOctober 2017

EBS reduces fixed mortgage rates and extends 2% back in cash offer

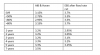

• All fixed rates reducing with the 3 year fixed down to 3.15% and 5 year fixed down to 3.25%

• €6,000 back in cash on a €300,000 mortgage

• Mortgage Masters to help people achieve their dream of home ownership

EBS today (Monday, 9thOctober) announced significant reductions in its fixed mortgage rates for new and existing*Private Dwelling home mortgagecustomers and the extension of its 2% back in cash offer for new mortgage customers.

All EBS fixed rates are reducing, with the 3 year fixed down to 3.15% from 3.65% and the 5 year fixed down to 3.25% from 3.80%.

The 2% back in cash offer has been extended to eligible customers, including switchers,whose mortgage draws downbefore 31st March 2018. EBS customers will continue to receive €2,000 back for every €100,000 in new mortgage borrowing drawn down.

EBS Chief Executive Des Fitzgerald said:

"Customers, especially first time buyers, have a strong appetite for cash offers in addition to very competitive mortgage interest rates.”

“Our back in cash offer has been very popular since we started it in June of last year. This extension of our offer, coupled with EBS’s reduced fixed rates offers great value to our customers.”

“EBS are the Mortgage Masters and our experts are on hand to help people achieve their dream of home ownership.”

The offer of 2% back in cash is available to customers taking out fixed or variable rate mortgages on Private Dwelling Houses, including first time buyers, customers moving to a new home, and customers who wish to switch their mortgage to EBS.

Fixed rate changes come into effect on 10thOctober 2017.

*If an existing customer is already on a fixed rate and wants to avail of the new rates an early breakage cost may apply.

I've just started a one year fixed rate at 3.5%. I'd better enquire about early breakage costs.

I've just started a one year fixed rate at 3.5%. I'd better enquire about early breakage costs.