Brendan Burgess

Founder

- Messages

- 54,757

This has come up in a few threads, and I think it would be worth teasing out separately.

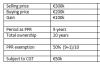

The CGT rules

If you sell your PPR within 12 months of vacating it, there is no CGT.

If you keep it as an investment, the CGT

If your house is worth less than you paid for it, when it ceases to be your PPR

If you paid €200k and it's now worth only €150k, any increase in value up to €200k is exempt from CGT.

If your house is worth today the same as you paid for it, but it increases in value while it's your investment property

So this is a tax-efficient investment

If your house is worth more today than what you paid for it, but falls in value before you sell it, you could end up with a CGT liablity

So, although your house falls in value while it is an investment, you end up with a CGT liability.

If you had sold it when it ceased to be your PPR, you would have avoided any CGT liability.

The CGT rules

If you sell your PPR within 12 months of vacating it, there is no CGT.

If you keep it as an investment, the CGT

If your house is worth less than you paid for it, when it ceases to be your PPR

If you paid €200k and it's now worth only €150k, any increase in value up to €200k is exempt from CGT.

If your house is worth today the same as you paid for it, but it increases in value while it's your investment property

So this is a tax-efficient investment

If your house is worth more today than what you paid for it, but falls in value before you sell it, you could end up with a CGT liablity

So, although your house falls in value while it is an investment, you end up with a CGT liability.

If you had sold it when it ceased to be your PPR, you would have avoided any CGT liability.

") , it's always a refresing way to view something differently.

, it's always a refresing way to view something differently.