I am hoping to buy a family house in the coming months. I have a investment property which is still in negative equity. I have however paid off a lot of the mortgage over the years and have a very nice tracker rate. Thankfully, I don't necessarily need to sell this property. It would however take a lot of pain away from our new mortgage. I will outline below some details and would appreciate any comments or advice.

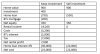

New house c. 900k

Savings 150k

Investment house worth 400k

1600 per month rent

Investment house mortgage remaining 200k (.75% tracker)

In simplistic terms I can either sell the house and get a 550k mortgage or keep the investment property and get a mortgage for 750k.

Myself and my wife, thankfully have very good jobs so can get either mortgage

New house c. 900k

Savings 150k

Investment house worth 400k

1600 per month rent

Investment house mortgage remaining 200k (.75% tracker)

In simplistic terms I can either sell the house and get a 550k mortgage or keep the investment property and get a mortgage for 750k.

Myself and my wife, thankfully have very good jobs so can get either mortgage

")