Brendan Burgess

Founder

- Messages

- 52,119

This report came out on 29th October. Surprised I didn't see it and no one else here seems to have noticed it either.

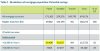

72% could cut their repayments by at least 10%

60% could save at least €10k over the remaining term of their mortgage

- Three in every five eligible mortgages stand to save over €1,000 within the first year if they switch mortgage provider, and more than €10,000 over the remaining term.

- Just 2.9% of mortgages switched provider in the second half of 2019.

- A diverse range of factors may inhibit switching, including psychological factors, lack of knowledge on the costs and benefits, and the perceived complexity.

72% could cut their repayments by at least 10%

60% could save at least €10k over the remaining term of their mortgage

Last edited: