Was browsing Revolut app this morning and found Savings menu. There were no email or push notifications about this. Also, cannot find this on their website.

Money are stored in Revolut Securities Europe UAB and not Revolut Bank UAB. So protection is 22,000 EUR.

Money are invested in Fidelity Money Market Fund.

Interests with Standard Plan (free):

EUR: 3.51% (1.86% net)

USD: 4.70% (2.42% net)

GPB: 4.67% (2.46% net)

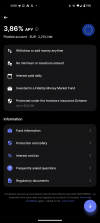

Interests with Metal Plan:

EUR: 3.86% (2.21% net)

USD: 5.05% (2.77% net)

GPB: 5.12% (2.91% net)

Interests with Ultra Plan:

EUR: 3.96% (2.31% net)

USD: 5.40% (3.12% net)

GPB: 5.27% (3.06% net)

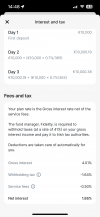

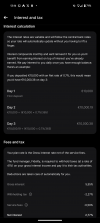

Tax at a rate of 41% is deducted automatically by Revolut.

Money are stored in Revolut Securities Europe UAB and not Revolut Bank UAB. So protection is 22,000 EUR.

Money are invested in Fidelity Money Market Fund.

Interests with Standard Plan (free):

EUR: 3.51% (1.86% net)

USD: 4.70% (2.42% net)

GPB: 4.67% (2.46% net)

Interests with Metal Plan:

EUR: 3.86% (2.21% net)

USD: 5.05% (2.77% net)

GPB: 5.12% (2.91% net)

Interests with Ultra Plan:

EUR: 3.96% (2.31% net)

USD: 5.40% (3.12% net)

GPB: 5.27% (3.06% net)

Tax at a rate of 41% is deducted automatically by Revolut.

Attachments

Last edited: