A common theme in these Statler and Waldorf (esque) 'charges' posts is what's left out of the posts. So, you end up with analysis by omission and fanciful comparisons.

This is a thread about

Occupational Pension Schemes - those can include a) individual AVCs (not PRSA AVCs) b) 1/2 person MT Executive Pensions c) to very large schemes with 1,000+ employees. So, don't post RAC/PRSA/PRB/ARF charges as there are plebty of non-disclosure (by poster/consumer) posts on those already.

There are no commission disclosure requirements on these schemes. There are charges disclosures and if you haven't been provided with them you can ask for them.

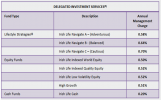

So, for the purposes of clarity and to focus on the tangible, can those who are claiming that their charges are too high on their occupational pension schemes please post i) the level of contribution you're making ii) the percentage the employer is making iii) the current value of your fund iv) the number of members in the scheme v) the AMC/Policy Fee/Allocation Rate (if you know there are early exit charges, include that) and vi) the number of funds available under the scheme. Also, if you think you have low charges, whether the employer is paying the administrator, separately, (say) €50,000 pa for the 'outsourcing' of that function.

If you're in a different jurisdiction (with a completely different regulatory/compliance regime) and are a member of a 'better' scheme, post ALL the actual details of the scheme as per i) to vi) above.

If you see a low-cost (exact same) occupational pension scheme product in another jurisdiction with all the charges quoted, provide a link to it so that we can see what you're talking about.

You've a better chance of someone helping you out if you include ALL the information from outset and it would really help those who read the

forum but don't contribute that much.

Gerard

www.prsa.ie