The reason you don't understand it, is because it doesn't make any sense at all.

It doesn't even start to make sense. So it's very hard to counterargue something like this.

Unfortunately, the Central Bank bought this argument. I presume that the Central Bank guys simply don't understand it, and rather than admit that, they just said "OK, AIB. We will take your word for it." They really should have referred AIB's explanation to an actuary who would have roared laughing at AIB's explanation.

Their argument seems to be

" If you pay the interest as it is due, then you were not charged interest on interest". This is very flawed.

It's easiest to explain with case studies.

Case study 1.

You took out a mortgage for €100k , 2 years ago at an interest rate of 4%.

You made no repayment at all.

If they charged you simple interest, today, you would owe €100k +€8k interest

But they charged you compound interest, so at the end of year 1, you owed €104k

They charged you interest of 4% of €104k or €4,160

So today you owe €8,160 interest.

Then you get a call from AIB to tell you that you made a capital repayment of €12,000 back 2 years ago and they forgot to credit it to your account.

According to AIB's Simple Interest approach, they will reduce your balance by €12,000 + interest @ 4% for 2 years or € 960

But in fact, in the first year, they charged you €480 interest.

In the second year, they charged you 4% of €12,480 or €499.20

So they owe you €979.20

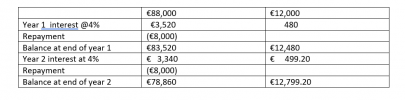

Case study 2.

You took out a mortgage for €88k , 2 years ago at an interest rate of 4%.

But AIB input it into the system as two loans - one of €88k and one of €12k.

You made repayments of €8,000 a year which they allocated against both loans proportionately.

Two years later, they discover their error and reduce your original balance to €88k.

AIB now argues that because the repayments exceeded the interest charged, you were not charged any interest on the interest.

This is disingenuous in the extreme. No other bank would try this argument.

This is what they should do:

They are refunding you €960 when they should be refunding you €999.20

Look at it another way...

AIB argues that as you paid the interest of €480 in year one, you were not charged any interest on that interest.

But you should not have been charged that interest. So you paid €480 in Year 1 which you should not have paid.

Therefore, in Year 2, they should pay you the interest on €12,000

And they should pay you interest on the €480 interest they charged you which they should not have charged you.

Brendan