Brendan Burgess

Founder

- Messages

- 55,428

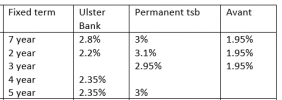

Ulster Bank is nearly the cheapest lender at the moment while permanent tsb is the most expensive. Anyone who moves to Ulster Bank who is not on a tracker will find themselves paying a lot more when they move to permanent tsb.

If you have a cheap tracker with Ulster Bank, you don't need to do anything.

permanent tsb will not be able to increase the margin.

If you have an LTV of less than 60%, you should switch to Avant now and fix for 7 years

The lowest rate with permanent tsb is a full 1% point dearer than Avant. So you should switch.

As mortgage rates will probably rise due to the fall in competition, then switching to Avant and fixing for 7 years seems appropriate.

"My mortgage balance is only €100k, is it worth switching?"

You can fix for 5 years with Ulster at 2.35% compared to 1.95% for 7 years with Avant. That is a saving of €400 a year for, say, 7 years or €2,800. It costs about €1,500 to switch. But you are probably going to face the cost of switching from permanent tsb anyway when your fixed rate is up. So, on balance, I would switch now and fix for 7 years.

"Avant is cheaper now, but how do you know they will still be good value when the fixed rate is up in 7 years?"

There is no way of being sure. But permanent tsb has a long history of keeping its mortgage rates very high for existing customers and getting new business through gimmicks like cashback. So it's very likely that Avant will be cheaper in 7 years.

But we know that they will be cheaper for the next 7 years.

If you have a loan to value of between 60% and 80% it's less clear cut

You can fix with Ulster now for 5 years at 2.45%. You could switch to Avant for 2.2%, a saving of 0.25% a year or 1.25% over 5 years.

On a €200k mortgage, that is €2,500. With legal fees of €1,500 up front, it might not be worth the hassle.

The only thing is that if you fix with Ulster Bank now, it is very likely that you will have to switch from permanent tsb when the fixed rate is up as they have a long history of charging high rates. No one knows, but I would guess that Avant will still be much cheaper than permanent tsb in 5 years.

If you have an LTV in excess of 80%, then fix with Ulster Bank now for 5 years

That is all you can do. If you don't fix now, you will be charged a much higher rate by permanent tsb.

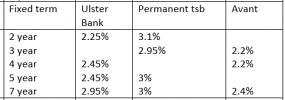

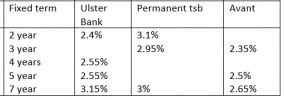

If you have a cheap tracker with Ulster Bank, you don't need to do anything.

permanent tsb will not be able to increase the margin.

If you have an LTV of less than 60%, you should switch to Avant now and fix for 7 years

The lowest rate with permanent tsb is a full 1% point dearer than Avant. So you should switch.

As mortgage rates will probably rise due to the fall in competition, then switching to Avant and fixing for 7 years seems appropriate.

"My mortgage balance is only €100k, is it worth switching?"

You can fix for 5 years with Ulster at 2.35% compared to 1.95% for 7 years with Avant. That is a saving of €400 a year for, say, 7 years or €2,800. It costs about €1,500 to switch. But you are probably going to face the cost of switching from permanent tsb anyway when your fixed rate is up. So, on balance, I would switch now and fix for 7 years.

"Avant is cheaper now, but how do you know they will still be good value when the fixed rate is up in 7 years?"

There is no way of being sure. But permanent tsb has a long history of keeping its mortgage rates very high for existing customers and getting new business through gimmicks like cashback. So it's very likely that Avant will be cheaper in 7 years.

But we know that they will be cheaper for the next 7 years.

If you have a loan to value of between 60% and 80% it's less clear cut

You can fix with Ulster now for 5 years at 2.45%. You could switch to Avant for 2.2%, a saving of 0.25% a year or 1.25% over 5 years.

On a €200k mortgage, that is €2,500. With legal fees of €1,500 up front, it might not be worth the hassle.

The only thing is that if you fix with Ulster Bank now, it is very likely that you will have to switch from permanent tsb when the fixed rate is up as they have a long history of charging high rates. No one knows, but I would guess that Avant will still be much cheaper than permanent tsb in 5 years.

If you have an LTV in excess of 80%, then fix with Ulster Bank now for 5 years

That is all you can do. If you don't fix now, you will be charged a much higher rate by permanent tsb.

Attachments

Last edited: