Sunnygirl69

Registered User

- Messages

- 165

Just wondering if any one else in Single Public Service Pension Scheme (new entrants) have AVC's with New Ireland? This was organised through Cornmarket, the trade unions agent of choice for some reason.

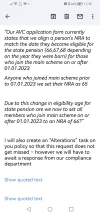

All my calculations were done based on a retirement age of 68 years. They appear to be unaware that current age for state pension is 66 years. I have attached a screenshot of what person I dealt with in New Ireland sent onto their compliance team. 5 weeks later I am still awaiting clarification on this. Not impressed with them at all.

All my calculations were done based on a retirement age of 68 years. They appear to be unaware that current age for state pension is 66 years. I have attached a screenshot of what person I dealt with in New Ireland sent onto their compliance team. 5 weeks later I am still awaiting clarification on this. Not impressed with them at all.