NoRegretsCoyote

Registered User

- Messages

- 5,766

The European Banking Authority published a report today on national insolvency frameworks across the EU.

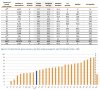

It shows Ireland has extremely low recovery rates for all sorts distressed debt: commercial, residential and SME.

See below gross recovery rate on non-performing mortgages. It's basically how much is retrieved by the bank through the formal debt recovery process. For Ireland it is 12%, about a quarter of the EU average.

Anyone who thinks this is unrelated to Ireland's very high interest rates is fooling themselves.

It shows Ireland has extremely low recovery rates for all sorts distressed debt: commercial, residential and SME.

See below gross recovery rate on non-performing mortgages. It's basically how much is retrieved by the bank through the formal debt recovery process. For Ireland it is 12%, about a quarter of the EU average.

Anyone who thinks this is unrelated to Ireland's very high interest rates is fooling themselves.